Tarrifying Times

What should we make of the announcement by Trump to pause the tariffs on China by another 90 days? Relief? Another example of ‘taco’, the idea that Trump will constantly u-turn on trade policy?

While Trump’s constant backflipping on trade policy does mean that his erratic policymaking being somewhat predictable, it doesn’t make an economist’s job any easier when it comes to predicting how tariffs might impact the economy.

I recently read a piece which spoke about the difficulty in predicting how tariffs might impact the economy. With the way Trump has threatened tariffs, pulled them back, changed this, and changed that, that might seem blatantly obvious. But when you are forecasting the impact of a policy, such as tariffs, you need to have some kind of assumption that underpins the forecast.

So, do you assume the tariffs that Trump announces? Or assume no tariffs at all because they will be pulled back? Or do you constantly update your forecast once Trump announces a new tariff?

The way markets are reacting, it seems most investors are assuming that Trump will always u-turned on policies. But the problem with this assumption, is even if Trump drops tariffs completely, his policies are still causing chaos. Moreover, even if countries are able to negotiate a deal, some form of tariff will remain on most countries. And the tariffs targeting certain industries don’t seem likely to go anywhere.

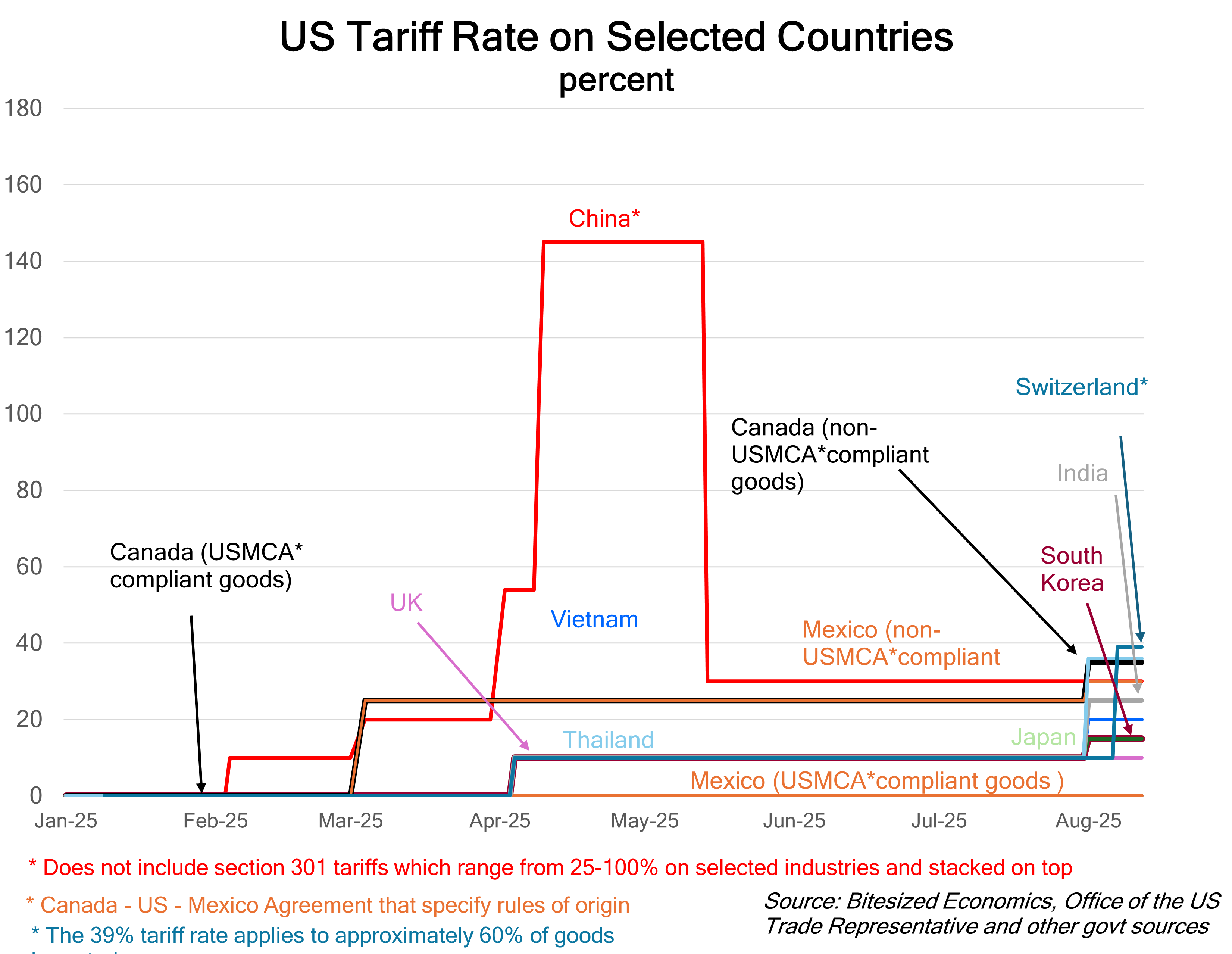

As an example of how complicated the US tariff structure has become, I created a couple of charts outlining tariffs by country and by industry:

Let me tell you this was not an easy task. It was incredibly confusing.

Firstly, there’s the question of how to treat tariffs which applied to some of a countries’ imports, but not all. For example, China has section 301 tariffs which apply to many of the goods from China, but not quite all. So, I decided to include these in the industry chart, rather than the country chart. Alternatively, the 39% tariff rate applied to around 60% of Swiss imports from August 7. Mexico and Canada have tariffs on their imports for non-USMCA-origin shipments (as part of the US - Mexico – Canada agreement) but not on compliant goods.

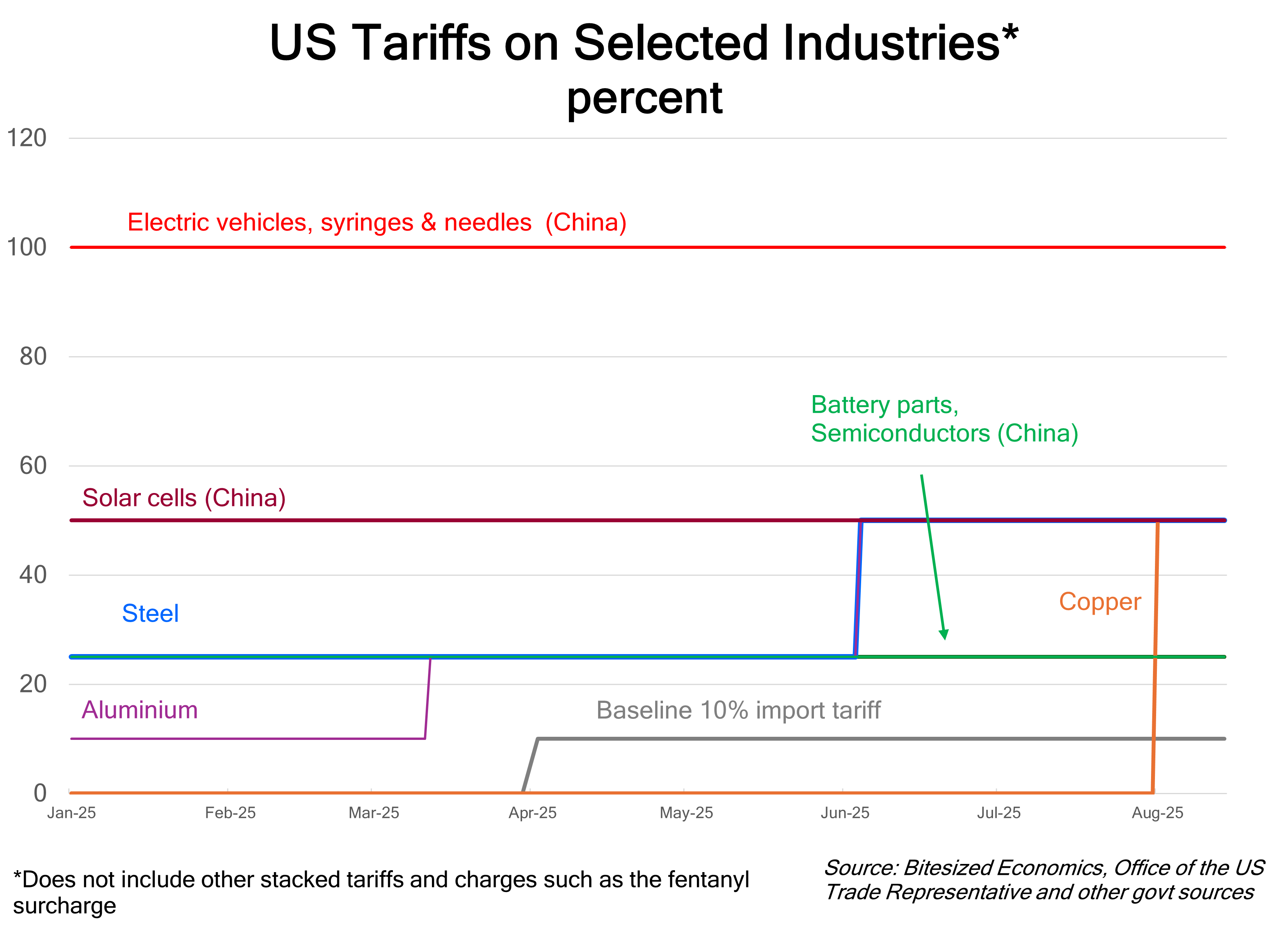

The tariffs on selected industries appears less complicated, but then there is also the question of which tariffs are stacked on top. The fentanyl surcharge for China is stacked, but the Mexico and Canada fentanyl charges are not. Steel and aluminium imports are exempt from the ‘reciprocal’ tariffs being stacked on top. BUT derivative products, ie. products which contains a metal (aluminium, steel or copper), have the aluminium, steel or copper component tariffed at 50%, and the other component at the country reciprocal rate.

Complicated?

You bet.

I’m just creating charts to illustrate a point, but what if those tariffs directly impact your business? How do you work out the tariff rate applied? Is it the country tariff? What if different parts are from different countries? The whole exercise is even more difficult when tariff rates could easily change next week.

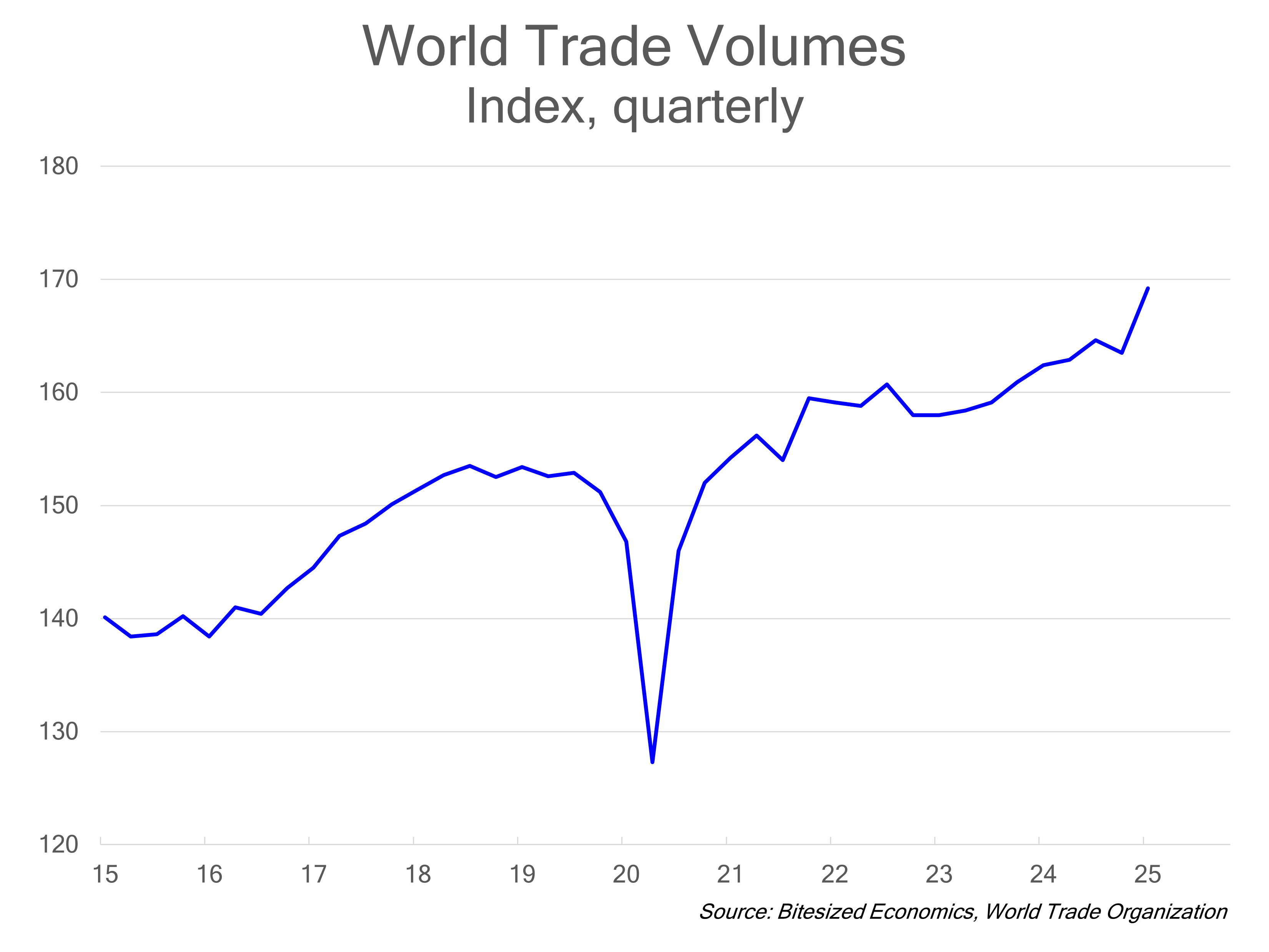

The fact that tariff policy has become chaos is already a major impediment to global trade, even you believed Trump will reverse course and ends up lowering the more stringent tariffs at the end of the day.

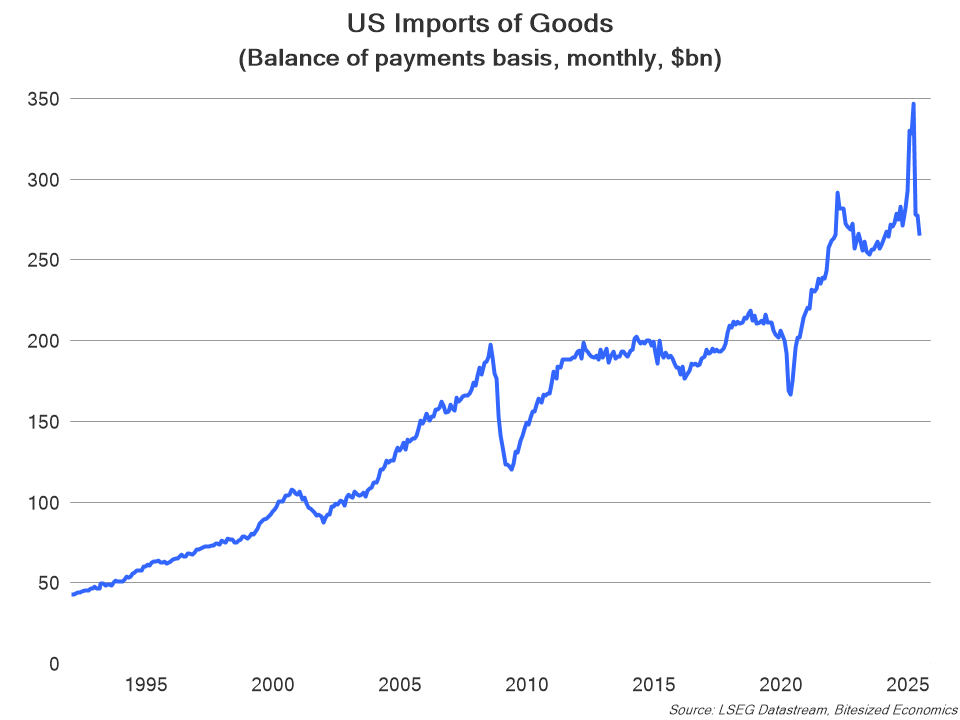

However, to date, world trade has not diminished significantly. Somewhat counterintuitively, trade volumes have actually increased, not decreased.

So, what’s going on?

In the past few months, imports to the US spiked prior to Trump’s liberation day announcement, although they have fallen back in more recent months.

But this pull-forward effect can’t last, as it reflects suppliers buying up ahead of the expected tariffs. Indeed, it will likely exacerbate weakness in trade flows over coming months.

Investment Implications

Investors have been quite relaxed with regard to trade amid hopes of trade agreements with major trading partners. But we have yet to see the pull-forward impact of US imports fully unwind. Further, the added complications to the world trading system is a constraint and adds a layer of red tape which will be negative for global growth over a longer-run time horizon.

Will this disruption affect earnings and sentiment eventually? Most likely yes. But a sharp downturn or recession isn’t on the cards just yet. The near-term focus is going to be on the US Federal Reserve and the prospect of rate cuts which should be positive for risk and sentiment.

**********************************************************************************************************

If you like this, and would like to see more insights do subscribe. And to show additional support I would be extremely thankful if you become a paid subscriber:

Alternatively, you can provide a one-off donation through my buymeacoffee link.

https://buymeacoffee.com/januchanD

All contributions are much appreciated! Thank you to all who have subscribed, shared and donated.