The problem with thinking the Strait will be open soon

I am no military or war expert.

I don’t want to try and predict what will happen in Iran.

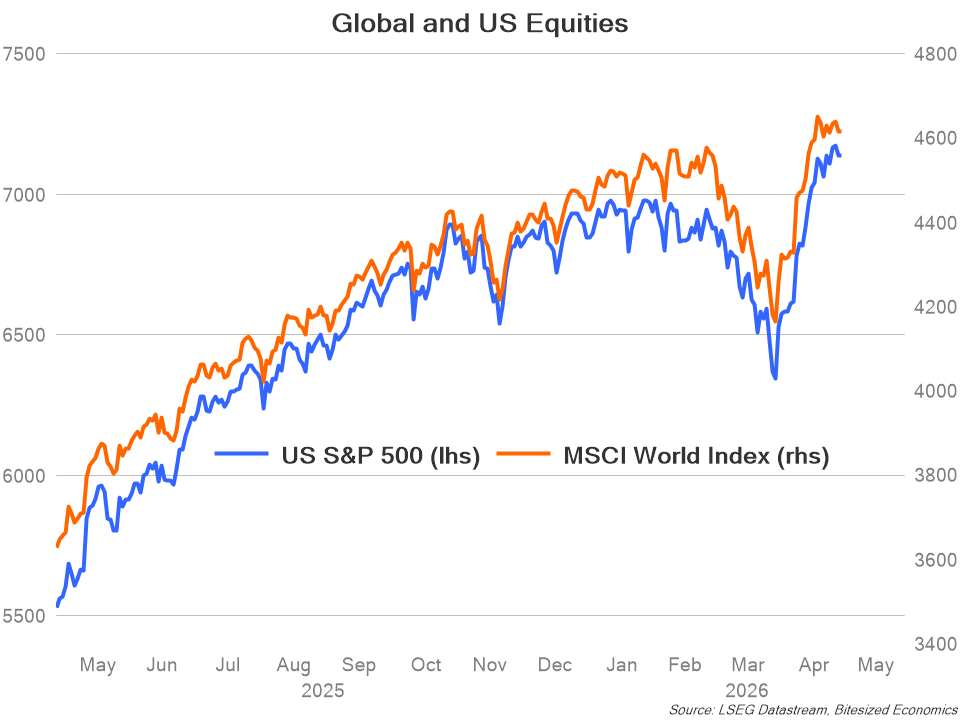

But it does seem to appear that financial markets still think that this won’t be a long- lasting war.

US and global equities are roughly back to where they were before strikes on Iran began in late February.

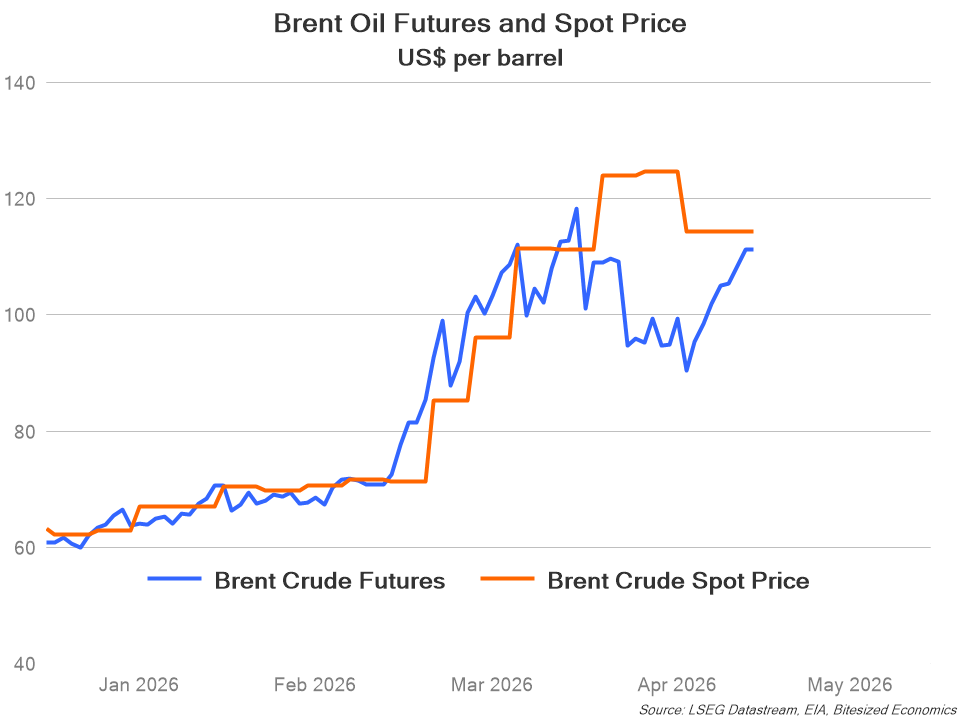

And while the physical oil market remains under strain with still very little traffic transiting through the Strait of Hormuz, the paper market is thinking differently. A divergence between the futures oil price and the spot price also suggest that the oil market is also expecting that the closure of the Strait of Hormuz isn’t going to be long-lasting, although that gap appears to have narrowed of late.

Financial markets could be right, and we all want them to be right.

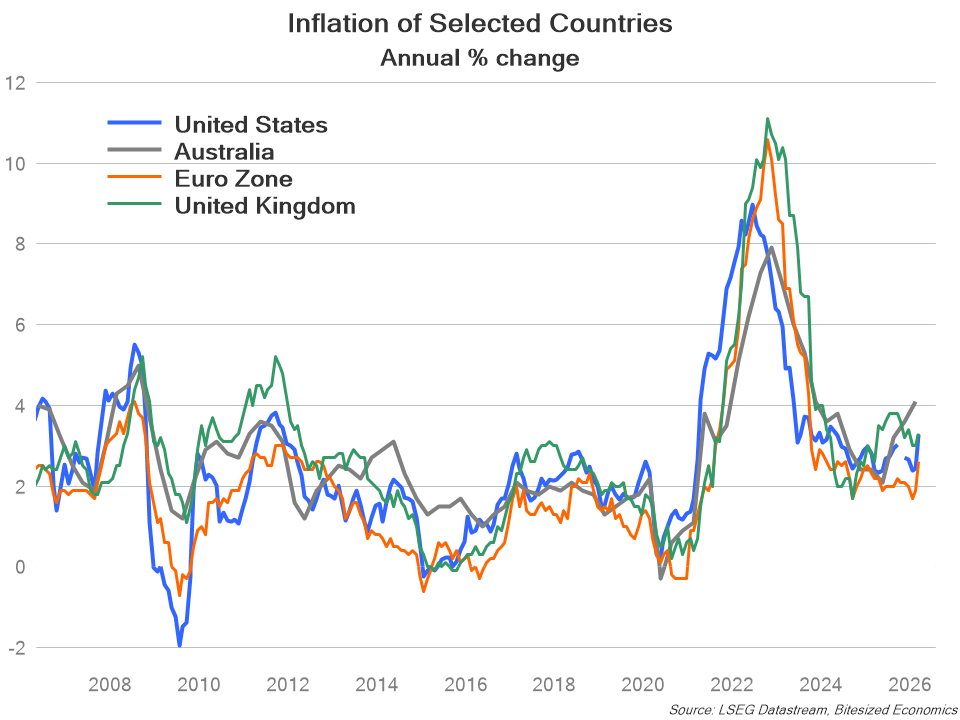

Of course, no one can say for sure what will happen. But what we do know is that whatever happens from now, energy costs are much higher, and that inflation is going to lift or has already lifted above inflation targets of central banks.

Inflation in Europe, the UK, the US and Australia have headed higher in March and now sit above their respective central bank targets.

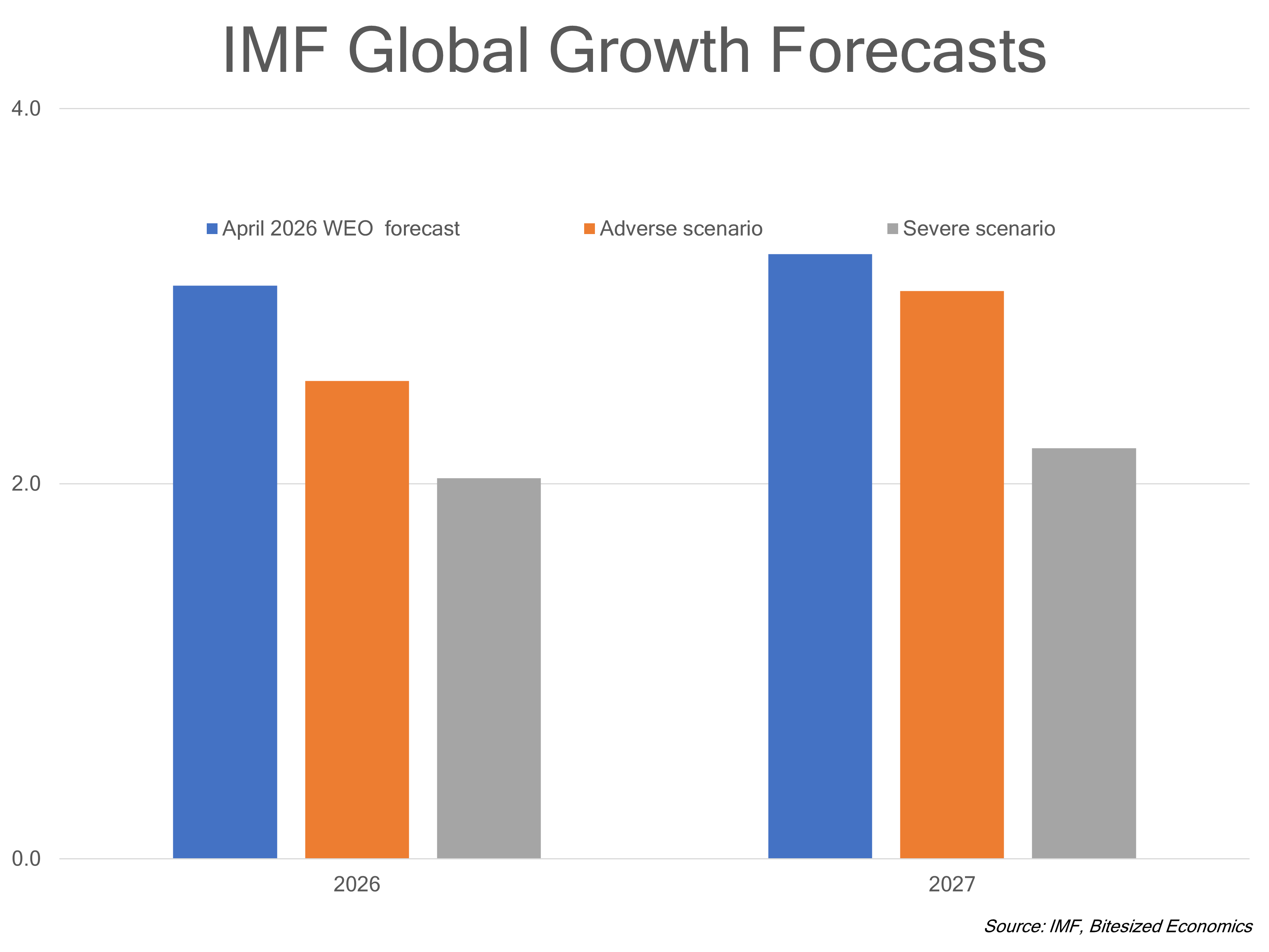

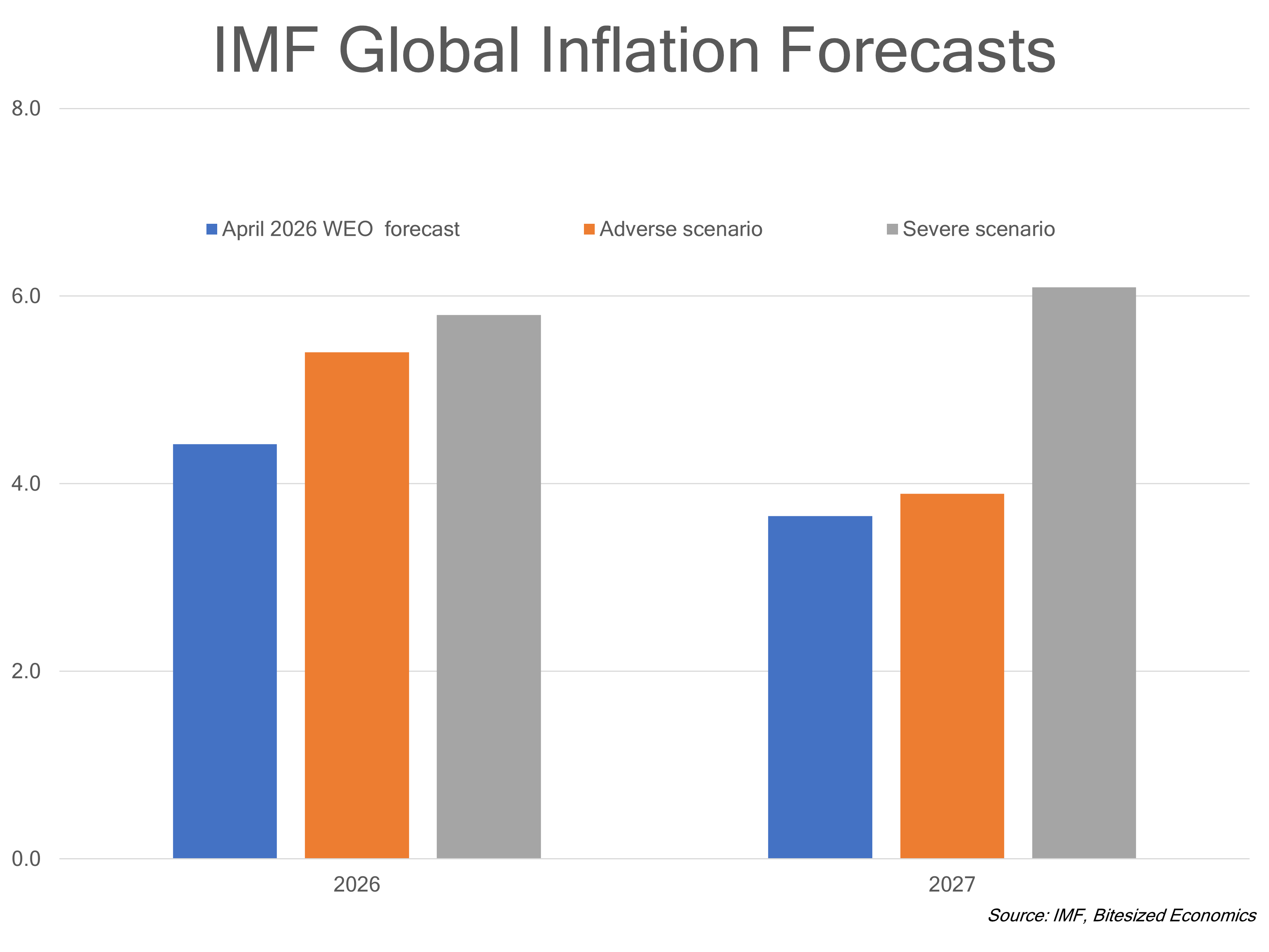

Meanwhile, the IMF have provided a baseline scenario of global inflation averaging above 4% for this year.

And inflation is just the tip of the iceberg. There are real concerns about securing enough fuel, energy and food supplies.

The big question is what should be done about it? Specifically, what is the ideal response from governments and central banks to an energy crisis and an inflation spike?

When the public faces rising costs, the obvious choice for authorities might seem to be provide help when it can. Provide support to households and give the people some relief. Already, governments have provided direct assistance, fuel subsidies or reductions to fuel taxes. Australia and many countries across Europe have reduced taxes, while Japan and China have provided some form of fuel subsidies.

For central banks which target inflation, it’s a bit of a tricky spot. Higher oil prices are going to hurt growth for most economies, but trying to support the economy by keeping down interest rates because of a supply crunch and runaway inflation tends to make the inflation problem worse without much benefit of growth. The best way to approach monetary policy depends on whether the shock is of a short-term nature, or more longer lasting. Generally, central banks can look through short-term supply shocks and inflation does come back down on its own. But the more persistent inflation becomes, the more likely it feeds into inflation expectations, inflation spirals become more likely and the risk increases that inflation becomes entrenched.

Officials from the Fed, ECB and the BOJ are more alert to inflation risks in their rhetoric, but central banks have held off from acting on stronger inflation outlooks.

This comes back to the point that the world’s base case scenario is that the conflict will end soon and that the disruption to energy markets will not be long-lasting.

But what if it is longer lasting? Wars tend to be unpredictable, and last longer, even though the intention of all parties is for a short conflict.

What if, traffic through the Strait of Hormuz doesn’t flow for six months, or even longer? And even beyond that, supply takes longer to recover?

Along with their baseline forecasts, the IMF proposed various scenarios for growth and inflation for an adverse scenario reflecting a “longer shutdown” and a severe scenario where “supply dislocations extend into next year”.

In a severe scenario, estimates for growth are close to 2% globally for both 2026 and 2027. That’s not necessarily global recession but its close, and it would be a severe slowdown.

But the problem with this kind of downturn is that inflation is expected remain high – the IMF expects inflation to sit at 6%. Even if central banks want to look through the inflation impact from the war, they are not going to be in a position to be cutting rates to support growth.

Conversely, the Fed and others will need to consider raising rates with a major supply constraint that is lasting longer than anyone thought – similar to the covid pandemic. The supply shock may be temporary, ie. inflation transitory, but then there is the question of how long transitory is going to be tolerated. If the war were to last much longer, central banks could be at risk of being behind the curve in raising rates and may need to lift them higher than they otherwise would.

That being said, there is a strong argument to wait given the uncertainty to wait because we don’t really know whether this is going to be a persistent supply shock. But the point of this piece is that if we don’t really know, a severe supply shock is likely possibility, and we’re not prepared for it.

In the case of governments, they would also find themselves in a difficult spot if the supply shock is more long-lasting. Do they continue the cuts to fuel taxes or subsidies? If so, they become a much bigger fiscal burden and can offset the appropriate demand response such as using alternative sources of fuel or energy.

And because of the uncertainty with the war, we aren’t going to see the usual supply response to higher prices because of the long lead times to ramp up production elsewhere.

Public statements from oil and gas companies in North America have suggested little new plans to invest despite higher prices. And in a survey of executives in the energy sector conducted by the Dallas Fed anonymous responses in a survey of energy executives further highlighted the difficulty in making plans because of the uncertainty. As one respondent said, “Hard to make long-term commitments or to “drill, baby, drill.”

Some respondents thought that the jump in oil prices would be temporary.

Meanwhile, another respondent said, “The divergence between paper barrels and physical is ironically large enough to steer a tanker through. It’s unclear if government entities are trying to steer the paper market down….”

It raises another problem with the futures market trading below spot – it could further worsen the supply and demand imbalance. Plus, it’s the physical market which matters for the global economy, not what traders decide what the price to be.

We may see an end to the war soon, or at least get the Strait of Hormuz open soon, like many seem to believe, what financial markets seem to believe and what we all hope to be the case.

But if we don’t, then we could be in much more economic pain than if the world had prepared for a prolonged conflict. Interest rates could higher than they need to be if central banks could have acted pre-emptively. Governments would be in much worse fiscal positions, especially if they felt the need to persist with support to households and businesses. And most importantly, we are not seeing the appropriate demand and supply response within energy markets.

No one wants to be the panicked chicken running around saying “the sky is falling”. But this current supply loss of oil, and other commodities is extremely significant, and is lasting longer than what anyone thought.

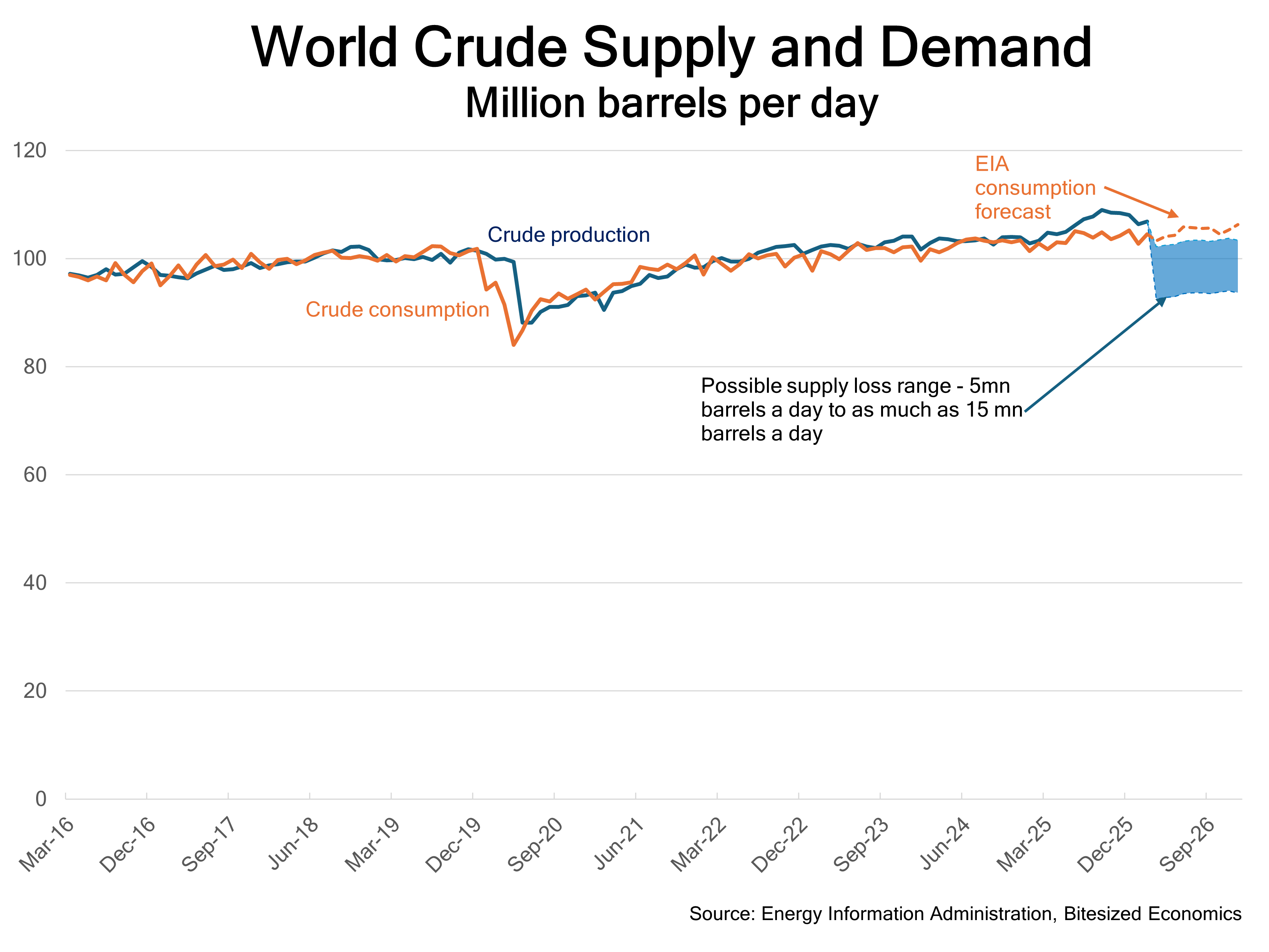

Upon the beginning of the war, here is the chart that I produced, thinking that a worse case scenario (the loss of 15mn barrels per day) seemed unthinkable.

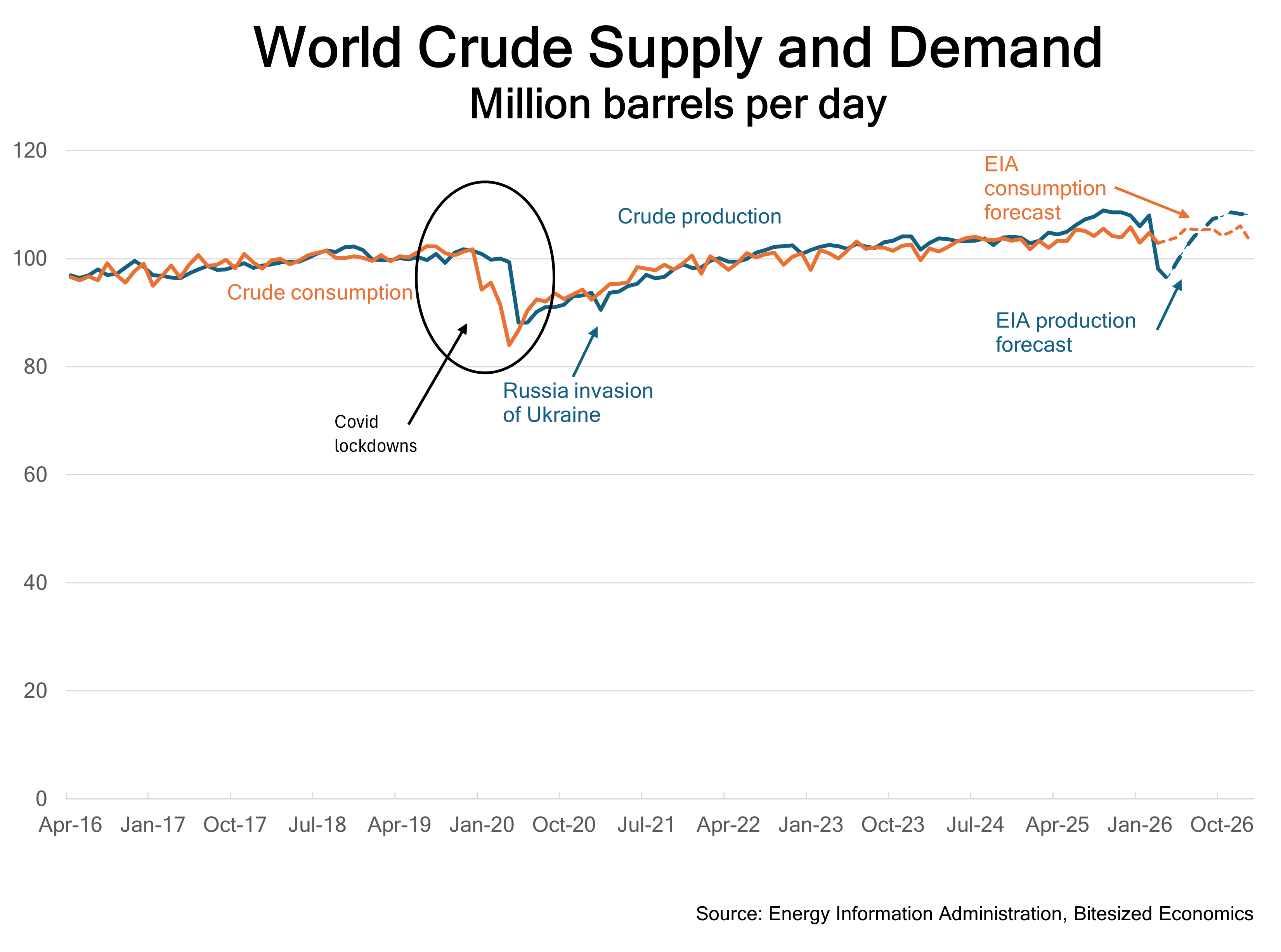

What has actually happened?

Here is an updated chart with the latest EIA data:

March and April are now looking at a production loss of between 9-11 million barrels per day from February’s production levels. That wasn’t the worst-case scenario, but it’s within the more pessimistic end of the range.

Moreover, the baseline forecast assumes production begins increasing by May and the supply demand imbalance resolving by August. That seems like an optimistic scenario. And even then, you can see that this outcome is still a supply drop close to what we saw in covid, and worse than the beginning of Russia’s invasion of Ukraine. It’s amazing that oil prices are not closer to $150-$170 per barrel.

But everything is hinging on the belief that the Strait will not be closed for too long. And no one wants to think of the alternate outcome.

I guess, maybe I should just be burying my head in the sand, just like everyone else.

The paper-versus-physical gap is where this gets interesting. Futures market is pricing a policy assumption. Everyone calibrates to the short conflict and the physical cost compounds in the background while the world waits for August. That's the part that worries me.

And 6% inflation? Yikes. Just read that UAE is leaving OPEC too, so self-interest filling the vacuum while uncertainty sits on the table feels like exactly the dynamic you're describing. Thanks for writing this, Janu.