What tariffs would really mean for the global economy

Welcome to the first piece of 2025. I hope it has been a restful festive season, because already, 2025 is proving to be eventful.

I’ll have to admit, when it comes to financial markets, thinking about this year brings me a touch of anxiety. US equities are looking really expensive after two consecutive years of 20%+ returns. Pessimism with regards to China’s economy is at an all-time low and other parts of the world, such as Europe, do not seem much better. Plus the US is about to get a president which will bring a whole lot of volatility.

One thing that probably has the world on edge is tariffs. The word has become almost as divisive as Trump himself and has any advocate of free trade up in arms.

There is plenty out there describing the perils of tariffs. They say tariffs will be a cost to the consumer. They say they will be inflationary.

But after some extensive pondering, here are some of my thoughts when it comes to tariffs:

Tariffs may not have as much impact on inflation and on the American consumer as much as some fear. But that is because tariffs may have limited impact of reducing the US current account deficit and bringing jobs to the US. Sure, there is the added administrative cost for businesses, and the additional uncertainty which would be a cost to the US economy. But when looking at the bigger picture, imposing tariffs disrupt a carefully balanced world system of trade and capital flows. In a world where the largest and most liquid capital market is in the US and with a flexible exchange rate, the easiest way for that system to adjust from large scale tariffs is through capital and the exchange rate, rather than trade flows. It takes time for production to shift to the US and for consumption to shift towards American made goods.

I have heard tariffs described as a de-facto devaluation, but if the US wants to maintain open capital markets and a flexible exchange rate, those market mechanisms are bound to offset the intended devaluation. Think of capital flows and the exchange rate as the adjustment of least resistance when it comes to tariffs.

That means for tariffs to have its desired impact of affecting trade flows and the US current account, it would only be effective if there is some restriction on capital and the exchange rate.

At some point, if the US gets really serious about reducing its current account deficit, talk may increase of a co-ordinated intervention to bring down the US dollar (a new Plaza Accord), or imposing capital controls. Both don’t seem very likely at this point, particularly the latter.

In a way, China may have done part of this job for the US, because it manages its movements in the yuan. There may have been the headlines about the yuan devaluing against the US dollar, but it has only depreciated around 4.5% since September, compared with a 9% appreciation in the US dollar index around the same period. Moreover, China will probably not let the yuan depreciate too quickly as it can exacerbate capital outflows.

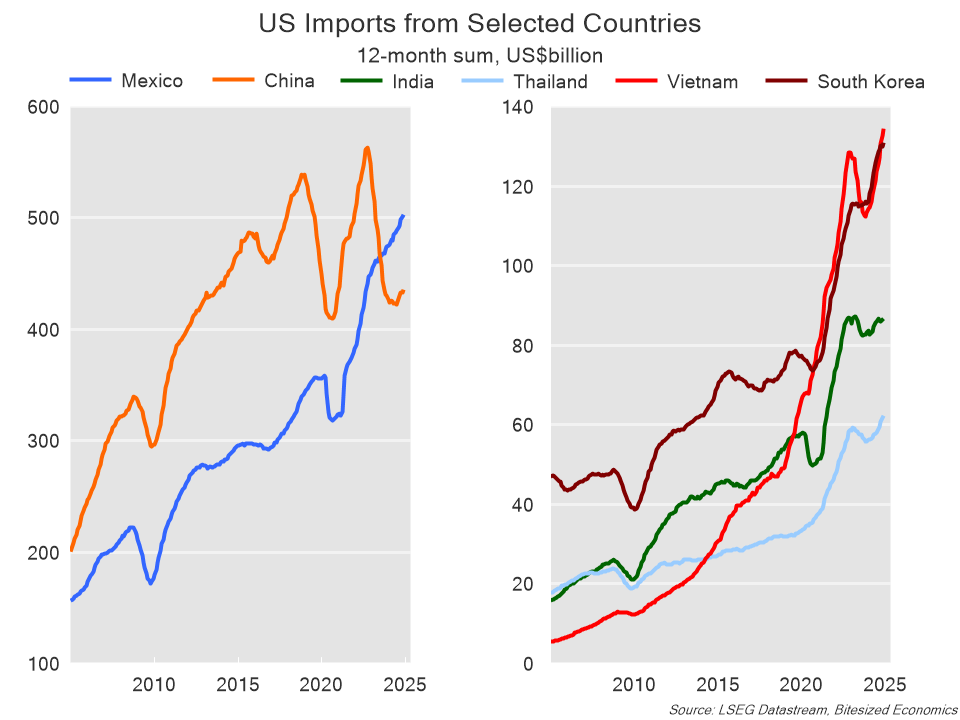

We have actually seen the US current account deficit against China narrow since tariffs were first introduced. But it hasn’t resulted in a reduction in the overall US deficit nor has it reduced China’s current account surplus with the rest of the world. That’s because trade has simply shifted to other countries. Imports may have decreased from China but simply increased with Mexico and other parts of Asia.

The Blanket Tariff

The diversion of trade, along with the offsetting movements in the exchange rate is why the tariffs targeting bilateral trade hasn’t worked to bring down the US deficit.

So, you can understand why Trump may want to bring in the tariff on all imports. A universal tariff would prevent imports simply being diverted to other countries. But there is no reason to expect that the blanket tariff would have a larger impact on trade flows and production in the US, and instead just have a larger impact on the US dollar.

The US dollar remains King

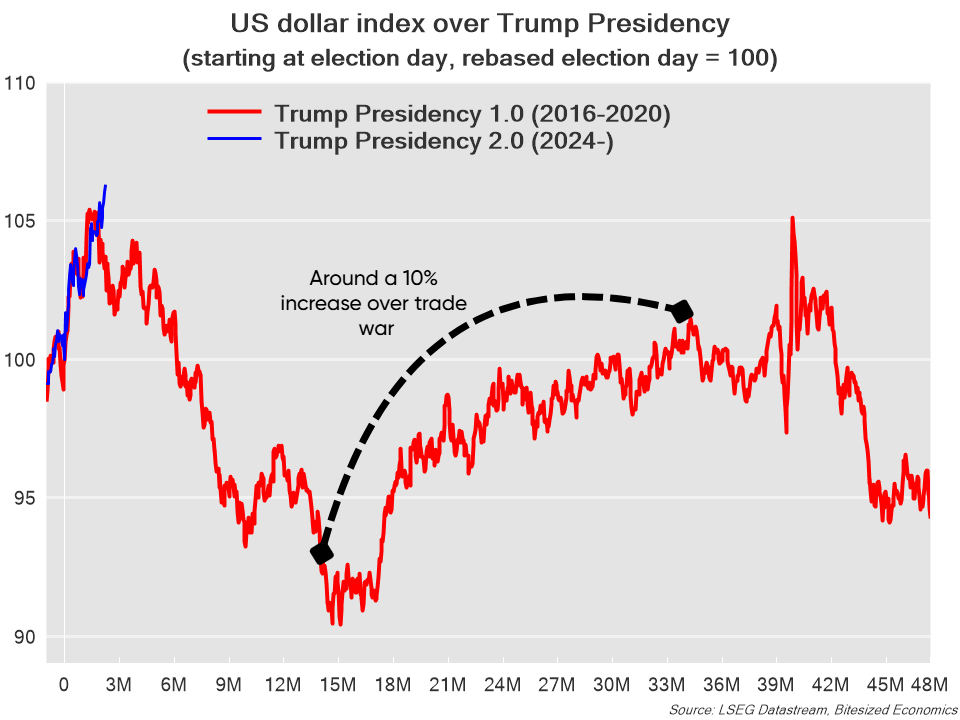

Of course, tariffs have been a big reason behind US dollar strength of late. Indeed, we’ve seen a remarkably similar trajectory in the US dollar as compared to Trump’s victory in the US election in 2016.

The big question is, given the surge in the US dollar since just before the election, are Trump’s tariffs already “priced in”?

With Trump tariffs this time around set to be bigger, including the proposed blanket tariff on all imports, it seems reasonable to expect a more pronounced appreciation of the US dollar to offset the tariff impact.

However, there are a couple of factors to consider this time around:

- the first round of Trump tariffs didn’t come into play until a year into his presidency. And it was exactly four years ago that the US dollar began a trend decline until Trump’s tariffs kicked off in 2018.

- We also have Fed policy and inflation to consider. There are bigger inflation concerns this time around, even though the unemployment rate is at a similar level to when Trump first started imposing tariffs in early 2018. There is less wiggle room for demand boosting measures without increasing inflation risks, but inflation concerns coming from Trump’s policies, particularly tariffs are likely to be overblown.

- Finally, we can’t forget what is happening elsewhere around the world. There is some extreme pessimism outside of the US, especially for China and also Europe, which means potential for big surprises on the upside.

Investment Implications

The US dollar is likely to trend head higher still, if Trump follows through with his tariff plans including the universal tariff on all imports. But be wary of periods of reversals given the uncertainty around the scale and timing of tariffs. Trump’s announcements on tariffs and also other potential policies are no doubt likely to be the key event risk for financial markets over the next few years.

US bonds are looking attractive given that inflation concerns with regards to tariffs and Trump’s policies in general are probably overdone. But the US economy is still looking mightily strong, that same resilience we’ve witnessed over the Fed’s entire tightening cycle. There is also probably something else going on beyond the strength of the US economy, which warrants some caution. But bonds could be a great buying opportunity if 10-year yields do hit 5%.

If you like this, and would like to see more insights do subscribe. And to show additional support I would be extremely thankful if you become a paid subscriber:

Alternatively, you can provide a one-off donation through my buymeacoffee link.

https://buymeacoffee.com/januchanD

All contributions are much appreciated! Thank you to all who have subscribed, shared and donated.

good breakdown janu